If the Coronavirus Pandemic of 2020 has made anything apparent, it is the sheer fact that Americans simply don’t save enough money.

While the pandemic has swept across the entire world and caused a global crisis, one thing that has stood out to many American adults:

Frankly, they don’t have enough in savings.

Not enough saved to live for 3-6 months due to unexpected reasons, let alone enough saved for retirement.

Depending on what financial expert you talk to, the general advice has been and will always continue to be you need to save 10%, ideally 20% of your income.

And while that might mean you need to do some math on your part, the real question you might be asking is “What amount of money should you have saved at your age?”

That is the exact question I asked myself at age 30. Not knowing the answer, I searched:

“How much should I have saved by age 30?”

What I quickly learned that was there are a few actual measurable/quantifiable/actionable numbers you can implement to save enough for retirement and to live a great life. And knowing those numbers is key!

- Savings by Age

- Retirement Savings Charts by Age

- How Much is Enough For You By Age?

- Saving Automation

- Tips for Saving Money

What should your retirement savings by age look like?

To add in my text : Self employed, Vanguard, Mutual fund, Individual retirement account, Boomers, Retirement fund, Retirement goals, Social security benefits, Withdraw, Retirees, Retirement income, Retirement account, Savings plan, Saving for retirement, Retirement savings

Most of us save (or should save) for four reasons:

- Emergencies (job-loss, illness, pandemics)

- Wants & Goals (new home, kids going to college, new car, trip)

- Retirement

- Security

In the article Americans Suck at Saving, the first thing you will recognize besides the blunt title is that the average American adult is saving less than 5% of their income.

In fact, for adults in their 20’s, who should be saving 25% of their income (less responsibility like kids, saving for college, etc) were saving less than 3% on average.

Simple math, 25% of someone’s gross income who is in their 20s would be $15,000 per year if they make $60,000 per year. This includes contributions to 401K’s, individual retirement plans and even debt repayments in addition to cash (liquid) savings.

Savings and financial expert Susan Orman of CNBC Money was quoted saying,

70% of the population has less than $1,000 saved.”

Whether that is you or not, after saving $1,000 as fast as possible, recognizing how much savings by age bracket you should have is essential. Setting retirement savings goals starts with setting appropriate saving benchmarks:

Age 30: Annual gross salary saved.

Age 35: Have 2x your gross annual salary saved.

Age 40: Have 3x your gross annual salary saved.

Age 45: Have 4x your gross annual salary saved.

Age 50: Have 5x your gross annual salary saved.

Age 55: Have 6x your gross annual salary saved.

Age 60: Have 7x your gross annual salary saved.

Age 65: Have 8x your gross annual salary saved.

Knowing that by age 40 you should have 3x your gross annual salary saved for retirement is one thing, but seeing what that would look like for a couple with a combined gross income of $100,000 is even better:

Age 30: $100,000 saved.

Age 35: $200,000 saved.

Age 40: $300,000 saved.

Age 45: $400,000 saved.

Age 50: $500,000 saved.

Age 55: $600,000 saved.

Age 60: $700,000 saved.

Age 65: $800,000 saved.

Setting appropriate savings goals by age is vital to your long term savings plan, which is why many savers often look for savings chart to help guide them!

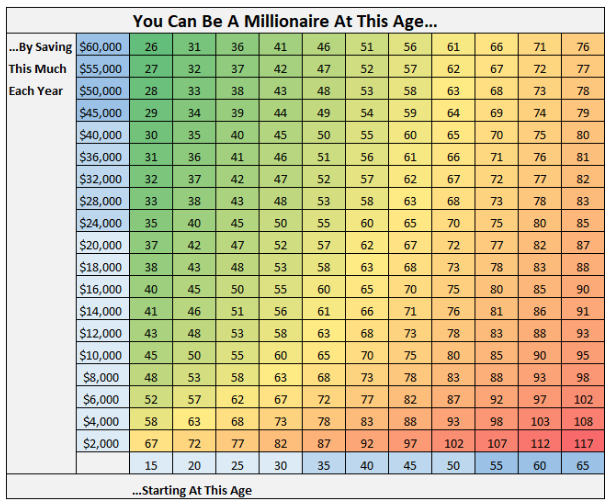

Retirement Savings By Age Chart

Whether you’re behind the savings curve when it comes to age or way ahead of it, using retirement savings by age chart will help guide you.

However, the elusive, magical savings number most covet is still the one million dollar mark. This savings chart was featured on CNBC Money and displays the steps to save to a million based on age:

The savings chart is simple to use:

- Along the x-axis you will find ages, starting at 15

- Along the y-axis is the amount to save annually to reach a million

- So if you start saving at 40, and want to retire by 65, you would need to start saving at least $16,000 a year, or $1,333 per month

- Hence – the importance of starting early

- Or if you are 40 and wanted to retire by 50 you would want to make sure you are saving $24,000 per year which equates to $2,000 per month.

The article goes to point out that the average person can be a millionaire within 30 years by saving just $833 a month. On the other hand, considering the fact that 1 in 2 doesn’t even have a $1,000 in savings combined, saving $833 a month might be a stretch for some people.

While the chart might simple to use, teaching yourself to save money might not always be a walk in the park, especially if you have not created a savings habit. Later we will explore saving ideas from daily challenges – to monthly saving guides – there is something out there for everyone.

[Related Content: 17 Ways to Cut Spending & Create Cash Flow.]

How Much Savings is Enough for You by Age?

How much do you want to be saved and what age do you want to reach that number?

Do you want to have:

- $2,000,000,

- $1,000,000,

- $750,000

- Or do maybe you just want $20,000 for a new car?

The answer to the savings question still boils down to what is the best number for you and your family’s needs.

While saving a million might sound cool, maybe right now you are just looking to create a nice emergency fund then dump some money into an annual vacation fund.

To know how much you need to be saved, consider working backward from your end goal. For example, consider long term financial goals, travel, retirement age, kid’s college and so on.

Personal finance and investment experts typically recommend planning to live on 80% of your income during retirement.

The same couple who made $100,000 earlier, would want to have approximately $80,000 per year to use for retirement. $80,000 per year equates to $800,000 for 10 years, and $1.6 million for 20 years.

Therefore, do your best to pick a number on the chart that is accurate and that can actually provide you with enough funds to comfortably retire! Having enough saved is key to retirement account withdraws!

Real Numbers: Average Savings By Age

We have firmly established that most do not have enough saved. That is OK consdiering awareness is key to creating any new habit – and saving is a habit.

That being said, you might be asking what do people really have saved by age? Below you will find the average median savings levels by age as of June 2019:

Source: Federal Reserve, FDIC, and MagnifyMoney estimates, June 2019.

Factors to consider with all numbers (aside from being arbitrary) is the bottom 40% of American households have little to no savings (less than $1,000). Conversely, the top 10% of the population by income is likely to have many times the national household savings average, thus mean averages are not as accurate.

While median averages are more accurate for measuring retirement savings by age, in the end the only focus for savings you should focus is on is climbing up the savings chart for yourself!

Tips to Help You Save More Money

You have to save more money, that is clear – we all do. Whether you’re in your 20s, 30s, 40s or quickly approaching reitrement, it is never too late to save.

Keep in mind, saving money is a habit, and it is a good habit to start at any age, especially if you’re just starting your career. On the other hand, even if you’re considered older by age, practicing saving is a good habit for when you do retire.

Automate Your Savings

So how do you take the headache out of savings? Do it automatically.

Whether you just can’t get yourself to manually take $250 out of every paycheck and stash it away or maybe you just spend all your money before you can save, set-up automatic savings.

The simplest way to save is to use direct deposit when available.

Using the savings by age chart, earmark a savings amount to go right towards your retirement savings or cash savings account. This takes the emotions out of savings and you almost forget you are even doing it.

Other automatic savings tips include:

- Use direct deposit to automatically save

- Take advantage of 401K employer matches – it is free money

- Use spar change apps like Acorns to round up purchases and save

- Open up a Vanguard brokerage account and use dollar-cost averaging

- Check out M1 Invest to use a robo-advisor

- Save your raises! Since you already use a budget, automatically save your raises in increase retirement contributions!

Acorns is a great app that will round up every purchase you make to the nearest dollar, stockpiling the difference in an investment account. At the end of the month, the stockpile is applied to a targeted item – in this case saving or investing.

For example, let’s say you use Acorns and you buy a burger next week for $4.25. After everything is all set up .75 cents would be added to your accumulating fund that then would be applied to your savings at the end of the month.

Use the Cash Envelope System

Saving money has less to do with “Saving” and more to do with your spending!

The average baby boomer has more saved because they were raised by parents who saw the repercussions of the Great Depression of the 1920’s.

While they certainly didn’t have to worry about student loans, unfettered lending, and raising healthcare costs, the boomers have practiced better savings habits than most.

And that started with their spending habits. So in order to help you curb your spending habits to save more money, consider using the Cash Envelope System if you’re not disciplined enough to save enough and need to cut back on spending.

How it works:

- Denote money for each variable expense, like groceries, gas, eating out.

- Place budgeted cash in each envelope

- Once an envelope is spent, that is it for the month.

- If there is extra at the end of the month, save it or use it for the next month

Other Saving Tips

A $1 in the market doubles every 10 years on average/historically.

$100 becomes $200, $200 becomes $400, and by year 30 that same $100 is now $800. Now, imagine that on a larger scale compounded over time with regular contributions?

Consider applying these quick saving tips to help you:

- See how much you’re saving now. Increase it by 1-2% every few months to give yourself time to adjust

- Fully fund a 6-12 month emergency fund

- Use employee matched retirement accounts that are tax-deferred

- Research dollar-cost averaging – contributing monthly to investments regardless of markets.

Final Thoughts on Savings by Age

So here is the savings by age takeaway… start saving more than you are!

If you’re under 50 and you think social security might be around, think again. The pandemic might end social security as we know it according to many financial experts and economists.

If an 18-year-old walked up to you right now and asked “What should I do with my money for the next 10 years?” you would tell them to avoid debt, save 75% of their income and live as cheap as possible.

On the other hand, if a 30, 40, or 50 year old asked the same question OR if you asked yourself, I hope the answer would be similar!

While living off 25% of your income is not feasible, saving 25% is!

Depending on your mindset, it is never too late to start and even saving 10% of your income is higher than the 2017 American saving rate of 3%.

Save more – live better might be the Walmart slogan, but it is also a great strategy for your financial future and savings by age!

Just remember, every dollar saved is doubled every 10 years in the market! Your future self will be glad you read.

This post was originally published on Money Life Wax and republished with permission.